The US is Priced for Perfection with Trump in Charge

Valuations, Trump and the general level of hubris are all making me nervous

This is not investment advice. It is my opinion only and is not a recommendation to buy or sell any stock or investment product. You should do your own research and invest according to your own financial circumstances.

I don’t want to dwell too much on Trump as this is a newsletter focused on the UK. But what America does influences us all so there’s only so much you can avoid it. I recently wrote about how the level of government spending has been an underappreciated aspect of US growth over the last decade. I thought I’d focus now on what I feel is an underappreciated aspect of markets today – how expensive US markets are.

This isn’t a big secret – they’ve looked expensive for years while continuing to roar ahead. And US stocks should trade at higher valuations than other markets given US companies have historically delivered higher earnings growth and been more profitable than other regions. Some premium, a quite large one, is justified even in normal times. Add to that an AI-induced earnings boom, and the concentration of big tech companies in the US, and it’s not difficult to justify where we are today.

Yet I follow things reasonably closely (without working in the industry day-to-day) and I still did a double take when I looked at the latest P/E ratio for the S&P 500.

And I did another when I looked at the longer-term Cape Shiller P/E ratio. People will endlessly debate whether this has any predictive value – and I personally remain somewhat scarred by making arguments against US equities c.2013 because the Shiller P/E was so high. Still, we’re at pre-1929 and pre-2007 levels today and that doesn’t feel comfortable.

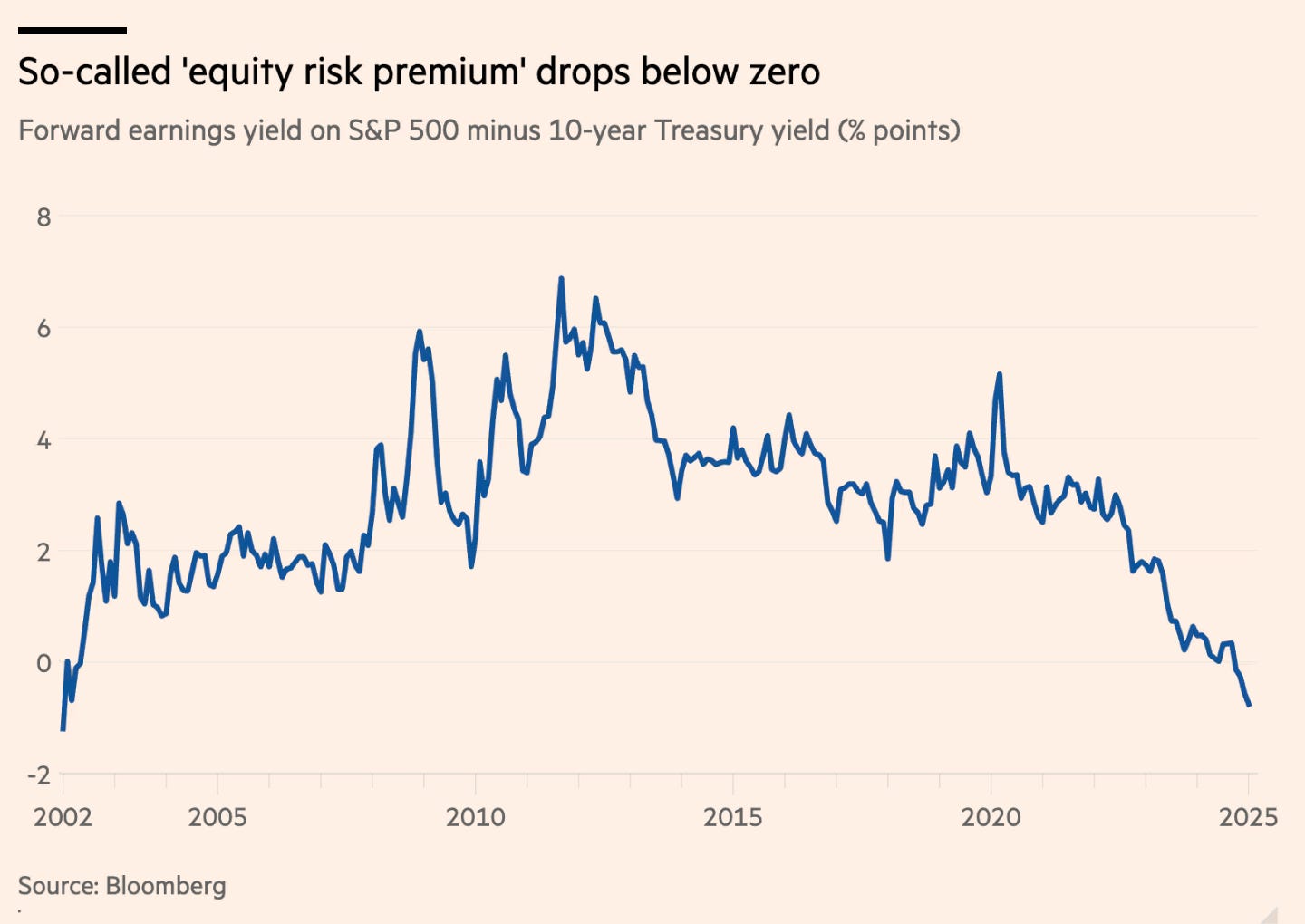

Then the FT had this chart of the equity risk premium, which compares the expected earnings yield on the S&P 500 to the 10-year Treasury yield. Again, we can endlessly debate what it means, but again, it doesn’t feel good.

Finally, my husband said forget about stocks – they can go to the moon, and you can “kind of” justify high valuations based on future earnings growth. Instead, look at credit spreads.

Currently the spread for US high yield borrowers (difference between lending to a risky corporate and lending risk-free) is ~2.5%, which is at levels close to before the financial crisis and before the blow-up of Long Term Capital Management in 1998. This is the tightest they’ve been in close to two decades, and unlike stocks, the price of bonds can only go so high (as you can only get par back). So credit spreads give a purer reflection of how much optimism is currently priced in (a lot).

It’s not just valuations that concern me though. As Keynes famously said, “markets can remain irrational longer than you can remain solvent”. Its valuations plus the sense of hubris in the air.

From an FT article on Davos:

Hours after Trump unveiled a blitz of executive orders, the same banker proclaimed that “everyone is all-in on America”. Summing up the prevailing mood, he said the next four years would be characterised by a “bonfire of regulations, ‘drill baby drill’, and the end of [environmental, social and governance] standards”.

From a different article on animal spirits:

The re-inauguration of Donald Trump as US president has ushered in a new period of “animal spirits” among business executives, as veteran investor Stan Druckenmiller put it this week. Chief executives are “somewhere between relieved and giddy” at the election result, he told CNBC. Meanwhile, US banks are in “go-mode”, a senior JPMorgan executive told the Davos crowd, while crypto is on the cusp of entering the “banana zone”, according to its boosters.

I don’t quite know how this ends, but it’s not hard to map out a few scenarios.

In one, a major tech company undershoots on earnings. AI’s transformative effect takes longer to emerge than imagined. The tech sell-off causes a rerating across the whole market, animal spirits are dampened, sentiment sours.

In another, inflation is still lurking, prices start ticking up more than expected, not helped by overzealous tariff and immigration policies. The Fed starts raising rates, Trump goes ballistic, Trump fires Powell, markets lose confidence in the Fed, rates rise further, Trump goes even more ballistic.

The first one may be a minor blip; the second could have wider ranging effects, as companies that shook off the first wave of interest rate rises following the pandemic – or simply postponed the pain – are now forced to realise losses. Defaults accelerate and credit begins to contract, as the US economy does too.

I’m not saying either of those – or some combination – are guaranteed to occur. But with US valuations where they are, there is little room for error. US markets looked priced for perfection.

And yet at the helm of all this is Trump. You can argue that the bark is worse than the bite, that they’ll be a lot of chest-thumping on tariffs and borders without a lot of action. It will be the NAFTA renegotiations all over again.

I’d argue that we just don’t know – and that that uncertainty is not fully reflected in valuations right now. Markets seem to be placing a lot more weight on actions that could be good for growth as opposed to ones that could be bad.

Sell the US, buy Europe and the UK then?

Unfortunately, not quite so simple. As Joachim Klement argued recently, a crash in the US won’t help European investors. But it doesn’t feel like going all in on the US is a good strategy right now either.

Oops! I swear I'd not even heard of DeepSeek when I wrote that

On bond spreads, is this not in part because of the US fiscal deficit, the record amount of issuance that’s coming, and the unwind of Yellen’s focus on the short end. So everyone is bearish treasuries distorting the ‘risk free rate’. When you look at the nominal yield on corporate debt it is attractive, especially in comparison to the expected return on equities at these valuations. I think there was another time when eg IBM debt was pricing inside government bonds.