Substack and the Future of Equity Research

A conversation on the decline of sell-side analysts and a new age for investor relations

This is a new type of post, where I tap up a friend or old colleague, to give an inside look on what’s going on in their industry. Like Nicolai Tangen’s podcast. Just less head of the world’s largest sovereign wealth fund meets CEOs of the world’s largest companies. More former low-to-middling employee meets current middling-to-senior employee. First up is a conversation with a friend who is a senior investor relations professional in the US where we talk about this recent article on Bloomberg, what social media means for the future of equity research, and how companies communicate with shareholders.

[Me]: Right, equity research. I’m interested in this because as you know I write a Substack, and I see a lot of people on Substack doing stock research. Some are hobbyists, some are former analysts, some are current portfolio managers. I wanted to talk a little about how the equity research model has changed and what that means for investor relations and the companies you work with. And since people on Substack LOVE reading about Substack, something on whether social media can help fill the void left behind.

[Friend]: Yes, sure. To give some background I’ve worked in investor relations for US companies for over twenty years. When I started, it was a different world. A free-for-all, but in a good way. If you were a small cap company, you could get covered by sell side analysts.

This changed after the financial crisis, but it was MiFID II that had the biggest impact1. It was an EU directive that decoupled research from trading. It wasn’t implemented in the US but everyone did it here anyway.

This completely changed the research business and really affected small cap firms. Banks just don’t make the ROI on covering small cap names, they’ll always choose a large cap name because people will buy that research.

As a small company your only chance of getting covered by the sell side is to sign up to a banking relationship. It’s costly, you’re paying for it, but you may get an analyst. Or you get lucky and someone at a small boutique writes about you, but that’s few and far between.

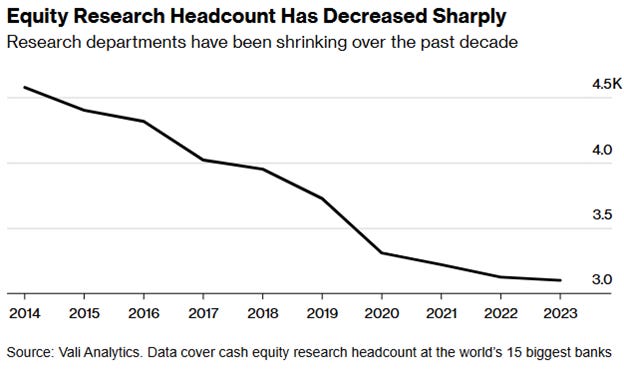

The main challenge is that there just aren’t enough equity research analysts anymore.2

Same story in the UK. The government even got involved and launched a review on investment research, which proposed some form of centrally provided research platform. I instinctively recoiled at this, although not sure the idea has gone anywhere since. Getting back to MiFID II though, how did that change the world of investor relations?

You need to do a lot more work. All the marketing to the sell side and buy side now falls on the IR team, whether that’s an in-house team (which smaller companies can’t afford) or outsourced. Even if you can get sell side coverage, they’re not setting up meetings with investors anymore. It’s hard to even get into the sell side run industry conferences as a small cap. Companies are more and more on the hook for selling their story.

Do you think this has impacted the make-up of shareholders in the companies you work with? And the valuations of the companies?

It depends a little on the company, but in lesser-known sectors, yes. Good equity research provides a thoughtful breakdown of a business. There can be a void with certain firms and sectors where investors just don’t how to value them.

I see it across small cap space, where it’s harder for companies to be valued properly. That’s so different from when I started, when even if you had only three or four analysts there was a diversity of voice and depth of understanding.

In theory that brings opportunity, especially for smaller investors. Small caps that aren’t covered may be more likely to be mispriced. But to realise a return you need other people to understand why they’re mispriced too... Reminds me of a conversation I had with a friend who is a buyside analyst, who was telling me about a small Japanese company he’d invested in. It was this incredible company but the share price kept going sideways. And then one day it popped out of nowhere and it was all because someone had posted on social media. It turned out to be a great performer, but absent the social media post (which is a total crapshoot), the share price probably would have just kept going sideways.

Ha yes. The first thing we do when we see erratic trading in a company is look on social media. Go to Yahoo Finance messenger boards and X, and see if anyone has posted something, good or bad, work out how to respond. In the past we’ve seen people post false information on these platforms, and in some cases, we’ve responded directly. But you can’t always do that because of SEC rules around materiality and disclosure. That makes it difficult to control a message at a time when you’re on the hook for doing more and more to present your story.

Which takes us nicely on to social media in general... Sounds like you’re not sold on social media being a replacement for sell-side research?

We go back and forth on social media and whether and how to work with influencers. It’s difficult to manage and there are very different levels of understanding. It’s also very hard to find influencers – they need a certain level of followers to make it worthwhile engaging from the company side, but what gets the most followers on social media often comes with risk. You don’t want to do an interview with a CEO and have it end up as a meme 24 hours later.

I see some good stuff on Substack but also a lot of generic stuff, and at the end of the day it’s targeted at individual investors. Do companies even want a big retail following, or engage with a retail investor base?

That’s changed a lot in the last few years. During the pandemic people had money to spare, were sitting at home, and traded a lot of stocks. Because there was money flowing, companies wanted to engage directly with retail. It was a wild west but also very innovative. Companies would do a traditional earnings call for institutions, then another on Clubhouse for retail investors. Others were doing YouTube videos. But that’s all gone away. No one even mentions Clubhouse anymore. Does it still exist?

No idea. I was never “cool” enough to get an invite when it was “cool” to get one.3

I remember begging someone to get me access… Anyway, your question on whether companies even want a retail following, that varies. It can be very unpredictable when you have a lot of individual investors. There was a consumer company I worked with a few years back… a well-known name but the following was incredibly volatile and it wasn’t helpful.

I do think companies need to talk to individual investors regardless, via social media and other platforms. But the company needs to take charge of that more. What you have is a blurring of investor relations and communications and marketing, whereas before they were more separate. IR and comms teams really need to work hand in hand today.

One thing I’ve come across in the UK is company sponsored research. Edison is one of the biggest firms and FT Alphaville wrote about it recently, noting that if FTSE 100 listed British American Tobacco (BATS) needed to pay for coverage, things must be really bad on the sell side. Although they made a good point that the issuer paid model is standard in fixed income (e.g. Moody’s and S&P). I find these reports can be quite helpful in setting out the industry and the business model, although I’ve yet to encounter one with a sell recommendation…

Well quite. In the US, company sponsored research started to become a thing a few years ago, but it’s never fully taken off, which I think is because of the impartiality point – the company is paying for a good presentation of itself.

It’s also quite expensive. Sidoti and Telsey are two big firms, but you’re looking at $50k pa, possibly $100k pa, for one initiation report plus quarterly earnings updates, which can be material for smaller firms. It’s good for an initiation report but is normally very mediocre for earnings analysis.

Biopharma and biotech use it a lot because of the niche nature of that industry, but for the types of clients I work with, I’d normally advise them to put the money towards a banking relationship with a reputable firm.

Has the rise of index funds changed investor relationships?

Passive is tough. We typically call the largest shareholders off the back of any major announcements - M&A, strategy or personnel changes etc. Looking at lists today and we can end up with just three or four places to contact. We may reach out to the passive funds on proxy votes, but they mostly vote with ISS so often they’re not even interested then.4

It’s an interesting space though, in terms of how proactive passive funds should or shouldn’t be as shareholders. If you take Vanguard, it recently signed an agreement with the FDIC that reinforced its “passivity” on bank shareholdings i.e. it agreed that it wouldn’t vote against the status quo. The FDIC was worried that these firms had undue influence over a sector, given the scale of ownership. FERC is also looking at this in utilities.

So, final question. With the big change in research, and rise of passive, where do you see investor relations in five years? How can companies sell their story?

Well, Wall Street certainly isn’t going to start employing lots of equity analysts again. Substack - and other social media - can help fill the void, but they are a small part. Nothing can compensate entirely for the end of the sell side model. Rather, it’s down to companies to get their message out and explain their business. Be proactive in communicating with shareholders, put out a steady stream of content that can be accessed by all, be responsive and accessible, and have that much closer relationship between communications and investor relations teams.

That makes a lot of sense. I’m going through the FTSE 250 at the moment and even just looking at a firm’s website, you get a sense of which ones “care”. The good ones are telling their story, putting up an investment case, putting up recordings of a capital markets day. Others just throw up an annual report and some earnings releases. I totally agree that companies need to sell themselves more - especially so in the UK when it often doesn’t come easy to us!

MiFID II, implemented in 2018, is an EU regulatory framework enhancing financial market transparency and investor protection. The main impact on investment research was that it “unbundled” investment research from trade execution. Prior to MiFID II asset managers would pay broker commissions on trades and as part of that get access to research. After MiFID II they were required to pay for the research separately.

Research headcount has fallen from over 4,500 in 2014 to just over 3,000 today according to Bloomberg.

Unclear. The app still exists but users have cratered. Apparently I’m not the only one to ask what happened.

ISS is a proxy firm that advises institutional investors on how to vote. When I worked in investment management, the operations team would notify the portfolio management team of any proxy votes in portfolio holdings, and ask the PM how to vote. I never saw any other reply than “vote with ISS”.

Great article. The growth of the internet and these platforms could be a reason why passive performs better than active. Markets are efficient. Every one has access to the same information at all times. Nothing is hidden behind Bloomberg terminals and paywalls

Very interesting and informative reading. I may be a little naive but I hadn’t realised all the Edison articles are company sponsored. To be taken with a pinch of salt in future.